Geopolitical Shock

Iran conflict sends shockwaves through auto production and supply chains

As US and Israeli strikes trigger a near-closure of the Strait of Hormuz, the global automotive industry faces rising energy costs, fractured shipping routes, and production and supply chain disruptions that could last well into summer 2026.

On the morning of Saturday, 28 February 2026, the geopolitical makeup of the global automotive industry shifted with unusual violence. Coordinated US and Israeli strikes on Iran, culminating in the reported death of Supreme Leader Ayatollah Ali Khamenei and senior security officials, triggered a chain reaction in the world's most critical maritime corridor.

Within hours, Iran's Islamic Revolutionary Guard Corps was broadcasting warnings to vessels in the Strait of Hormuz that passage was "not allowed." By late Saturday evening, vessel traffic through the strait had fallen by approximately 70 per cent. Hapag-Lloyd, Maersk, CMA CGM and MSC, among others, had issued formal suspensions of their transits. The automotive industry's exposure to what follows is far-reaching, and in many ways it has been hiding in plain sight.

The strait is not, in the minds of most automotive executives, a facility of direct concern. Oil flows through pipelines and arrives at refineries. Parts come from suppliers. Components are assembled and vehicles are finished. The connection between a narrow waterway at the entrance to the Persian Gulf and a car assembly plant in Nagoya, Sunderland or São Paulo can seem abstract.

It is not. It is, in fact, one of the most important physical constraints on the industrial economy, and its disruption now lands squarely on the order books, energy bills and shipping schedules of manufacturers everywhere.

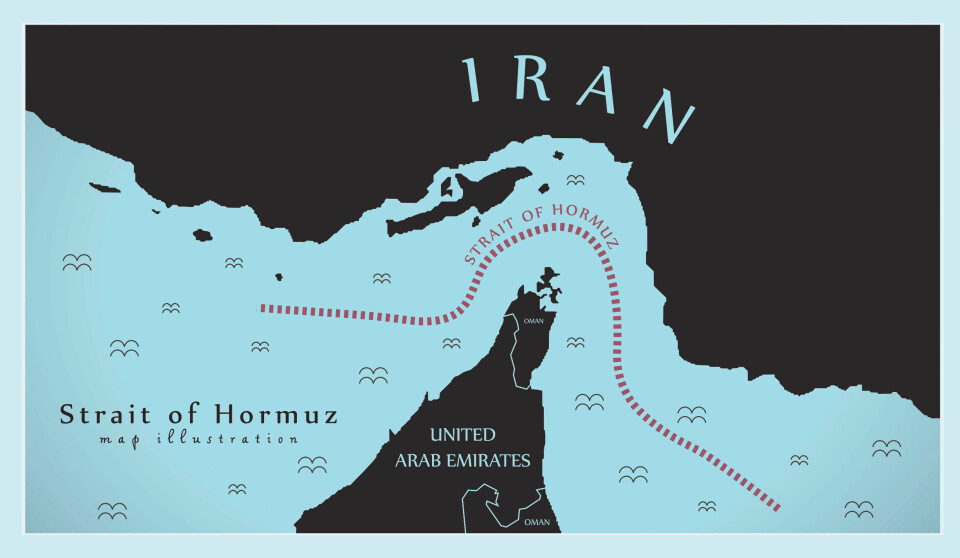

The chokepoint and the cascade

The Strait of Hormuz handles approximately 20 per cent of the world's daily oil supply and, crucially, 22 per cent of global liquefied natural gas exports, almost all of which originate in Qatar. About 20 million barrels of crude oil and petroleum products transit the waterway each day, serving Saudi Arabia, Iraq, Kuwait, the UAE and Iran itself. The corridor's narrowness, at its tightest point a mere 33 kilometres wide, is what makes it strategically decisive and operationally fragile.

Brent crude closed at $72.87 per barrel on Friday, 27 February, already elevated by weeks of mounting tension. Analysts are now projecting an immediate spike when markets reopen, with several forecasting prices in the $80 range should hostilities persist into the working week. In a worst-case scenario involving a protracted closure and Iranian strikes on Gulf Arab energy infrastructure, oil could reach $100 per barrel or beyond. "A prolonged closure of the Strait of Hormuz is a guaranteed global recession," warned Robert McNally, an energy analyst at Rapidan Energy Group, a view widely cited in market commentary as the crisis unfolded.

Global vehicle production braces for impact

For automotive manufacturers, the transmission mechanism is not complicated, but the consequences are wide. Energy costs account for a significant proportion of total production expenses in vehicle assembly. Steel foundries and aluminium smelters, whose output feeds every stamping line on the planet, are among the most energy-intensive industrial facilities in existence. Paint shops, body presses and powertrain machining all consume electricity at scale. When the marginal cost of energy rises sharply, the pain distributes itself throughout the supply chain within weeks, not months.

Plastics, rubber and the hidden cost of every vehicle

The modern vehicle contains roughly 150 to 200 kilograms of plastic components. Dashboards, door panels, bumpers, wiring harnesses, seals and fluid systems are almost entirely petrochemical in origin. The polymer feedstocks that underpin these components, ethylene, propylene and polypropylene, are derived from naphtha and natural gas liquids. Both are priced against crude oil benchmarks and both are transported through routes that now face direct disruption.

At a time when the automotive industry is struggling with a seeming permacrisis, including The Great $60bn EV Reset, the US-Iran war will not only have severe supply chain impacts, but also serious economic ramifications; higher energy costs, increased logistics costs, lower sales/production volumes, lower margins, and those inflationary effects feeding into higher interest rates, higher capital borrowing costs, further compounding already delayed investments

Market analysts have estimated that petrochemical feedstock cost increases of between 15 and 25 per cent could be expected in a sustained disruption scenario, forcing production adjustments and supply chain reconfiguration across plastics, adhesives and specialty chemicals. For a manufacturer producing several hundred thousand vehicles per year, this is not a rounding error, but represents tens of millions of dollars in additional input cost, with limited ability to pass it through to consumers already contending with inflationary pressure.

Rubber, similarly, is not immune. While natural rubber cultivation is geographically distant from the Gulf, synthetic rubber, which dominates tyre, seal and hose production in modern vehicles, is an oil derivative. Any sustained petroleum price shock ripples into synthetic rubber pricing within a matter of weeks.

Containerships going nowhere threaten carmaking

Beyond energy inputs, the immediate operational disruption centres on maritime logistics. Approximately 170 containerships, with a combined capacity of around 450,000 TEUs, were inside the Strait of Hormuz or its immediate approaches at the time of the initial IRGC warnings, according to analysis by Hua Joo Tan, co-founder of Linerlytica. Many are now effectively trapped.

Marco Forgione, Director General of the Chartered Institute of Export and International Trade, was unequivocal in his assessment of the supply chain implications. "Nothing will be transiting the Strait of Hormuz... that's oil and liquefied natural gas... will be stopped [and] global container shipping that transits through the region, that will be delayed and diverted."

He added that supply delays, "at a time when manufacturing remains highly integrated and 'just in time', would squeeze availability and cause price hikes." He estimated that it could take months for supply chains to reset, with effects persisting through the end of the first quarter and potentially into early summer.

The repercussions of the joint military operation by the US and Israel against Iran and subsequent retaliatory action will see the further weaponisation of trade and shatter hopes of a large-scale return of container shipping to the Red Sea in 2026

Peter Sand, Chief Analyst at maritime data firm Xeneta, drew a sharper geopolitical conclusion. "The repercussions of the joint military operation by the US and Israel against Iran and subsequent retaliatory action will see the further weaponisation of trade and shatter hopes of a large-scale return of container shipping to the Red Sea in 2026."

Carriers had been cautiously returning selected east-west services to the Suez Canal in recent months, following years of Cape of Good Hope rerouting prompted by Houthi attacks. Those plans are now shelved indefinitely.

For automotive parts supply chains, the physical geography matters enormously. Jebel Ali, in Dubai, is one of the world's principal hubs for automotive distribution throughout the Middle East and South Asia, and handles millions of vehicles and components each year. It sustained temporary disruption on Saturday after falling debris from an aerial interception caused a fire at one of its berths. Kuwait's port of Shuaiba was fully suspended and evacuated. Qatar suspended all maritime navigation. Bahrain halted operations at its main commercial port. The industrial implications of simultaneous shutdowns at Gulf hubs of this scale are severe.

Asian automakers face the sharpest exposure

The asymmetry of vulnerability in global automotive manufacturing is not random. It maps almost precisely onto oil import dependency, and that map runs directly through the Strait of Hormuz.

Japan imports roughly 90 per cent of its crude oil, and a substantial proportion of that volume transits the strait. Toyota, Honda and Nissan, which collectively manufacture tens of millions of vehicles annually across Japan and their global networks, face direct exposure to energy price shocks that compress margins at every link of their supply chains. Nippon Yusen, one of Japan's largest shipping groups, instructed its fleet on Saturday not to navigate the Hormuz corridor. South Korea, home to Hyundai and Kia, sources approximately 70 per cent of its oil from the Gulf. India, a growing manufacturing powerhouse and an increasingly important export platform, derives nearly half of its crude imports from the same corridor.

China, with approximately 84 per cent of the crude moving through Hormuz bound for Asian markets, stands as the most exposed major automotive economy. It is both the world's largest vehicle market and, through brands such as BYD, SAIC and Chery, an increasingly significant global manufacturer and exporter. A prolonged disruption to the strait would create simultaneous supply-side cost inflation and demand-side economic contraction. Samuel Ramani, Associate Fellow at the Royal United Services Institute in the United Kingdom, put it plainly. "That's going to have severe inflationary effects for the global economy," he warned.

The EV supply chain is not immune

There is a tempting but mistaken narrative that electric vehicle manufacturers, freed from dependence on combustion fuels, are somehow insulated from events in the Gulf. They are not. The battery minerals that underpin the EV transition, lithium, cobalt, nickel and manganese, are all energy-intensive to mine, refine and transport. Freight costs are a function of fuel prices. Smelting and processing costs, which dominate the economics of battery material preparation, track energy prices closely.

China controls over 80 per cent of global battery manufacturing capacity, and European battery makers, including the Korean-backed operations of LG Energy Solution, Samsung SDI and SK On, account for less than 10 per cent of the continent's operational production capacity. The vast majority of raw material flows that feed these facilities transit maritime routes either upstream of, or physically overlapping with, the Strait of Hormuz and the Indian Ocean shipping lanes now in question.

Insurance costs for shipping through the wider region are, according to Jakob Larsen, a former Royal Danish Navy commander and Chief Safety and Security Officer at BIMCO, likely to rise substantially. "We expect insurance rates to increase manyfold [and] ships with business connections to US or Israel approaching the area are probably not going to be able to get insurance," he said. An insurer's reluctance to write war risk cover for Gulf transits, even after hostilities formally subside, can effectively close a waterway as surely as a mine.

Rerouting around Africa

The alternative to the now-disrupted Suez and Hormuz routes is the Cape of Good Hope, and the arithmetic is not favourable for precision manufacturing. Rerouting via the Cape adds approximately 10 to 14 days to transit times for vessels travelling between Asia and Europe or the Americas. This is not a theoretical inconvenience; it is an operational transformation. Buffer inventories, already thinned by years of lean manufacturing philosophy and post-pandemic supply chain reform, are not sized for a fortnight of additional transit time in either direction. Assembly plants in Germany, the United Kingdom, the United States and Mexico will begin to feel the effects of delayed Asian component shipments within two to three weeks of any sustained closure.

Fuel consumption for vessels rerouting around Africa increases significantly, adding to both carrier costs and the broader carbon footprint of global automotive logistics. At a moment when OEMs are under increasing regulatory pressure to report and reduce their Scope 3 supply chain emissions, the grim irony is that a geopolitical crisis is forcing the industry to burn more fuel in order to avoid a different crisis altogether.

Manufacturing sites with high energy intensity, including smelters, foundries and surface treatment facilities, should be examining demand management options and any available contractual flexibility

Dylan Mortimer, Marine Hull UK War Leader at Marsh, identified the risk profile with clinical precision. "The primary risks centre on the Persian and Arabian Gulf, particularly the threat of vessel boarding and seizure by Iranian forces and the potential closure of the Strait of Hormuz," he said. The prospect of seized vessels is not hypothetical. In April 2024, Iran's Revolutionary Guard seized the Portuguese-flagged container ship MSC Aries in the strait, and the current operational environment is considerably more volatile than that episode.

When the guns go quiet, the costs linger

There are, in fairness, some stabilising forces at work. Global crude inventories are not at historic lows. OPEC spare capacity, primarily held by Saudi Arabia and the UAE, is being actively positioned for deployment, and both countries have bypass pipeline capacity that, in theory, circumvents Hormuz for a portion of their oil exports. Joseph Brusuelas, Chief Economist at financial services firm RSM US, noted on Saturday that "history has shown that the price increases are temporary and quickly revert back to near pre-conflict levels."

But the automotive industry's experience of the past five years counsels against assuming that supply chain disruptions are either brief or predictable. The semiconductor shortage of 2021 began as a 12-week problem and lasted two years. The Red Sea disruptions that emerged from Houthi activity in late 2023 were still constraining service patterns in early 2026, and carriers' plans to return to the Suez Canal this year are now indefinitely shelved. Structural disruptions to maritime logistics compound themselves through port congestion, equipment imbalances and insurance market rigidity in ways that persist long after the underlying trigger has been resolved.

Tom Kloza, Principal at Kloza Advisors, identified a specific mechanism that could sustain disruption regardless of whether the strait formally reopens. "The attack by Iran on other neighbors in the Persian Gulf changes the calculus," he said, adding that "the extent of the assaults put pressure on insurers to either aggressively raise tanker rates for Strait of Hormuz travel or balk at underwriting any traffic." That dynamic, once established, is slow to reverse. An insurer's appetite for war risk pricing is guided less by a stated ceasefire than by the re-establishment of verifiable security in the zone.

Daniel Harrison, Senior Automotive Analyst, Ultima Media

The cumulative economic impact may ultimately prove more destabilising than the immediate operational shock. Beyond delayed vessels and higher bunker costs lies a deeper financial strain that the industry is poorly positioned to absorb. As Daniel Harrison, Senior Automotive Analyst at Ultima Media observed:

“At a time when the automotive industry is already navigating a seeming permacrisis - including what has been described as The Great $60bn EV Reset - a US–Iran war would not only trigger severe supply chain disruption but also significant macroeconomic consequences. Higher energy and logistics costs would compress margins, while lower sales and production volumes would coincide with inflationary pressure feeding into higher interest rates and rising capital borrowing costs, further compounding already delayed investment decisions.”

In other words, even if physical trade routes stabilise, the financial aftershocks could linger far longer - reshaping investment cycles, capital allocation strategies and the pace of electrification.

What manufacturers must do now

The immediate response for automotive manufacturers is unlikely to be dramatic, but it must be deliberate. Procurement teams should be mapping exposure to Gulf-origin petrochemical feedstocks, assessing tier-two and tier-three supplier concentration, and modelling lead time extensions on the assumption that Cape of Good Hope rerouting becomes the default for at least the next six to eight weeks.

Energy procurement strategies calibrated for oil in the $60 to $75 range need to be reviewed. Financial hedging positions on energy and polymers, where they exist, should be reassessed for adequacy. Manufacturing sites with high energy intensity, including smelters, foundries and surface treatment facilities, should be examining demand management options and any available contractual flexibility.

Longer term, the events of the past 48 hours are another powerful data point in an accelerating argument for supply chain regionalisation, energy diversification and strategic inventory buffers that the automotive industry has been reluctant to fund in full. The efficiency logic that has governed global manufacturing for three decades has a powerful and recurring adversary, and its name is geopolitics.

Whether the current crisis resolves in days or extends into weeks, the structural message for automotive manufacturers is unchanged. The world's most vital waterway is no longer a background assumption. It is a variable, and it is now being actively tested.

Articles chosen for you...

-

Renault adds Bursa as second global Boreal production hub

-

Why Geely’s ECRI is focusing on collaboration, not just technology

-

Nissan, Chery explore Sunderland manufacturing partnership

-

SMMT warns new EU trade barriers threaten UK automotive manufacturing investment

-

VW reportedly weighs closure of four German plants in deepest cost-cutting push yet

-

GM Defense and Lockheed Martin forge production alliance

-

How Volkswagen wants to become more competitive again

-

Nucor's blueprint for low-carbon steel: EAF technology, scrap control and transparent reporting

-

Mercedes‑Benz Vans marks a new era with VLE production at Vitoria

-

Daimler Truck establishes umbrella brand for military business